PF2 - Short Squeeze Presentation

23

Short Squeeze Introduction and Examples PF2 Securities Evaluations 40 Fulton Street, 20 th Floor New York, NY 10038 (212) 797 0215 www.pf2se.com May 2015

-

Upload

gbphillips123 -

Category

Economy & Finance

-

view

1.418 -

download

0

Transcript of PF2 - Short Squeeze Presentation

Short SqueezeIntroduction and Examples

PF2 Securities Evaluations

40 Fulton Street, 20th Floor

New York, NY 10038

(212) 797 0215

www.pf2se.comMay 2015

Disclaimer

This presentation has been prepared by PF2 Securities Evaluations, Inc. (PF2). It is published solely for informational purposes,

it does not constitute an advertisement and it should not be construed to constitute a solicitation or offer to buy or sell securities

or financial instruments in any jurisdiction. No representation or warranty, express or implied, is provided with regard to the

accuracy, completeness or reliability of the information contained in this presentation, except with respect to information about

PF2, nor is this presentation intended to be a complete statement about or summary description concerning the securities,

markets or developments referenced in this presentation. Investments involve risks and investors should exercise their own

reasonable business judgment in making investment decisions. Nothing in this presentation should be regarded as a substitute

for the conduct of independent analysis. Any opinions expressed in this presentation are subject to change without notice and

may differ or be contrary to opinions expressed by PF2 on account of the use of different assumptions and criteria in a different

context. The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially

different outcomes. Those responsible for the preparation of this presentation may interact with trading desk personnel, sales

personnel and other parties in gathering and interpreting market information. PF2 is under no obligation to update or keep

current the information contained herein.

PF2 prohibits the redistribution of this material in whole or in part without the written permission of PF2 and PF2 accepts no

liability whatsoever for the actions of third parties in this respect. Copyright © 2015 PF2 Securities Evaluations, Inc. All Rights

Reserved.

2© Copyright 2015 PF2 Securities. All Rights Reserved.

Leverage & Margin

• Market participants use leverage to amplify asset returns.

• Just like putting 20% down upfront when buying a home, whenmonies or securities are borrowed and lent (to achieve leverage) theborrowing party often puts down an amount against the debt incurred(even if the debt is secured by, say, a piece of property).

• We call the amount that is “put down,” the margin.

• In our example, the home is the collateral asset securing the loan,protecting the lender if the borrower defaults on, or stops paying,mortgage payments. The lender could foreclose on the house, andsell it to recover the amounts owed on the loan.

• Now suppose the home is reappraised on a daily basis…

3© Copyright 2015 PF2 Securities. All Rights Reserved.

Margin & Buy-Ins

• If the home is reappraised daily, the value of the collateral securing the

mortgage changes each day.

• In theory, the lender is exposed to the risk that the home price

depreciates, in which case selling the home, if need be, might not cover

the lender’s outstanding loan to the home owner

• In the financial markets, where assets are valued regularly, lenders are

able to buffer against this risk: brokers require investors to put down more

margin when the value of the collateral/assets declines, or when the

borrower’s creditworthiness becomes an issue.

• The broker often “calls” the investor for more margin. It’s a margin call.

4© Copyright 2015 PF2 Securities. All Rights Reserved.

Margin Calls and AIG

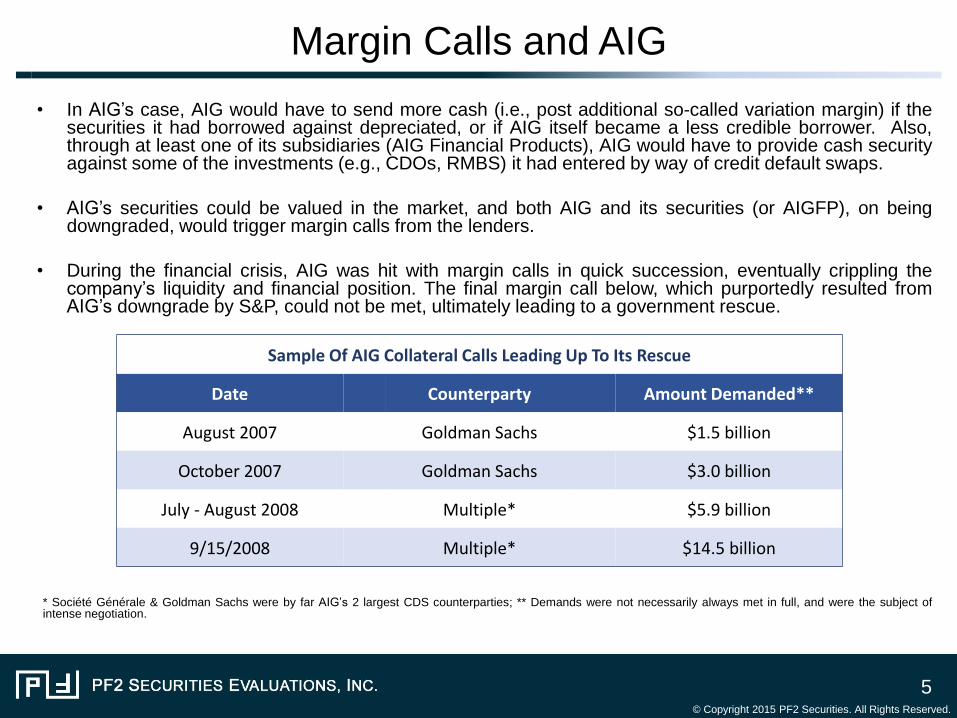

• In AIG’s case, AIG would have to send more cash (i.e., post additional so-called variation margin) if thesecurities it had borrowed against depreciated, or if AIG itself became a less credible borrower. Also,through at least one of its subsidiaries (AIG Financial Products), AIG would have to provide cash securityagainst some of the investments (e.g., CDOs, RMBS) it had entered by way of credit default swaps.

• AIG’s securities could be valued in the market, and both AIG and its securities (or AIGFP), on beingdowngraded, would trigger margin calls from the lenders.

• During the financial crisis, AIG was hit with margin calls in quick succession, eventually crippling thecompany’s liquidity and financial position. The final margin call below, which purportedly resulted fromAIG’s downgrade by S&P, could not be met, ultimately leading to a government rescue.

* Société Générale & Goldman Sachs were by far AIG’s 2 largest CDS counterparties; ** Demands were not necessarily always met in full, and were the subject ofintense negotiation.

5© Copyright 2015 PF2 Securities. All Rights Reserved.

Sample Of AIG Collateral Calls Leading Up To Its Rescue

Date Counterparty Amount Demanded**

August 2007 Goldman Sachs $1.5 billion

October 2007 Goldman Sachs $3.0 billion

July - August 2008 Multiple* $5.9 billion

9/15/2008 Multiple* $14.5 billion

Short Squeeze

A market participant who is selling “short” can be exposed to what we call a …

short squeeze

The way this works is a little tricky, and needs some initial background. We’ll first

explain what a short seller is, and how a short seller can be “squeezed.”

Next, we’ll detail some of the elements that can make a squeeze all the more potent,

potentially inflicting massive losses, and possible bankruptcies, on investors.

6© Copyright 2015 PF2 Securities. All Rights Reserved.

Introduction to Short Selling

• We need first to understand what a short seller is.

• An investor may wish to express a bearish view and profit from a decline

in an asset’s price.

• For example, an investor may think a stock is going down.

• Instead of “buying low and selling high,” short sellers aim to “sell high and

buy low.”

7© Copyright 2015 PF2 Securities. All Rights Reserved.

How Short Selling Works

• How does it work? An investor:

(1) borrows shares of the security from his broker

(2) sells those borrowed shares at current market price

(3) at some point in the future, covers his short by buying the shares

“back” and returning them to his broker

• Importantly, the investor has borrowed shares (or something else), and is

exposed to the risk that the price goes up quickly before he can replace

them, or “cover” his short.

8© Copyright 2015 PF2 Securities. All Rights Reserved.

Securities Lending

• Borrowing and lending of securities is a popular market practice.

• When it works well, securities lending increases marketplace liquidity,

thus lowering transaction costs and increasing market efficiency.

• However, securities lending concerns were central in the demise of

Lehman Brothers and AIG, among other banking failures.

9© Copyright 2015 PF2 Securities. All Rights Reserved.

Short Squeeze

• Now that we understand what a short seller is doing, what is the

squeeze?

• A short squeeze occurs when an initial rise in the security’s price causes

a large number of short sellers to try to cover their positions all at once.

• The scrambling to buy back the borrowed shares, causes the price to go

up further, exacerbating the pain felt by remaining short-sellers yet to

cover their shorts.

• The shares or asset prices can become completely divorced from its

intrinsic value while the squeeze is on.

10© Copyright 2015 PF2 Securities. All Rights Reserved.

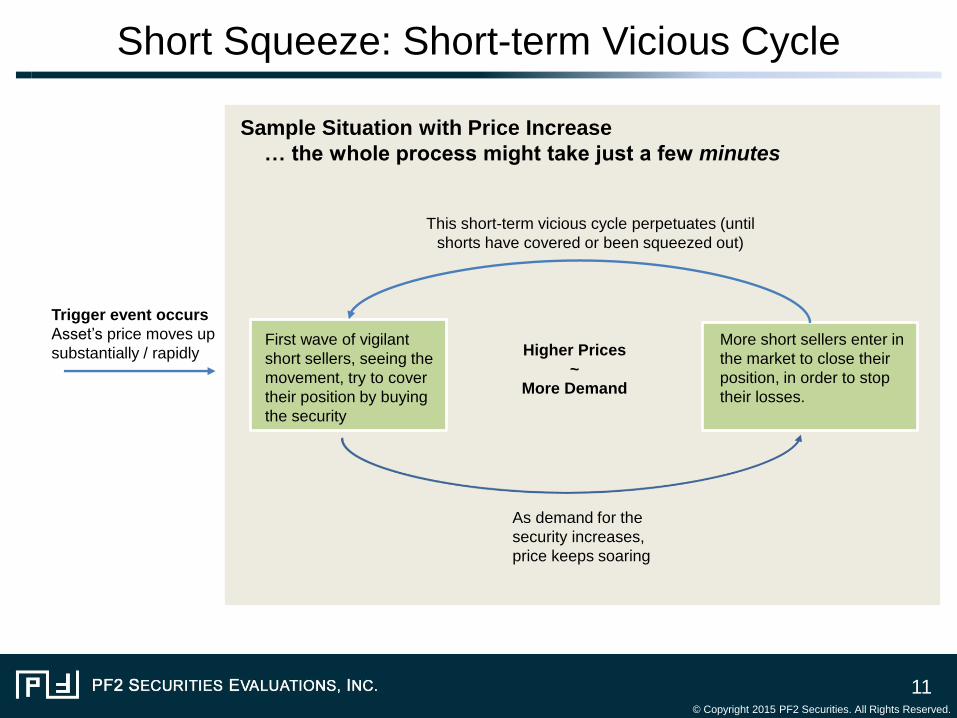

Short Squeeze: Short-term Vicious Cycle

11© Copyright 2015 PF2 Securities. All Rights Reserved.

Trigger event occurs

Asset’s price moves up

substantially / rapidly First wave of vigilant

short sellers, seeing the

movement, try to cover

their position by buying

the security

As demand for the

security increases,

price keeps soaring

More short sellers enter in

the market to close their

position, in order to stop

their losses.

This short-term vicious cycle perpetuates (until

shorts have covered or been squeezed out)

Sample Situation with Price Increase

… the whole process might take just a few minutes

Higher Prices

~

More Demand

Short Squeeze

• A key ingredient is the buy-in

• Investors may make rational (or irrational) short-covering decisions based on: new

information; aversion to greater losses; perceived value relative to price; perceived risk;

cost to borrow shares and hold short position; etc.

• The broker is indifferent. The broker will pay any price to cover the investor’s short.

This drives up the price even more, further eroding margin balances and triggering yet

more buy-ins, causing a greater spike as the asset’s price can become completely

divorced from its intrinsic value while short positions are covered.

12© Copyright 2015 PF2 Securities. All Rights Reserved.

Cost to Borrow (Debited from Margin Account)

• If stock is not widely available to borrow, broker will charge investor

interest on borrowed stock (borrowed amount calculated as number of

shares multiplied by current price per share).

• If stock becomes harder to borrow or “locate”, broker increases interest

rate charged, raising the cost to borrow.

• If stock price rises, then amount borrowed increases, raising the cost to

borrow.

• As rising borrowing costs make short position more expensive to

maintain, the short position can become uneconomical, thus providing

impetus to cover one’s short and perpetuating the upward price spiral.

13© Copyright 2015 PF2 Securities. All Rights Reserved.

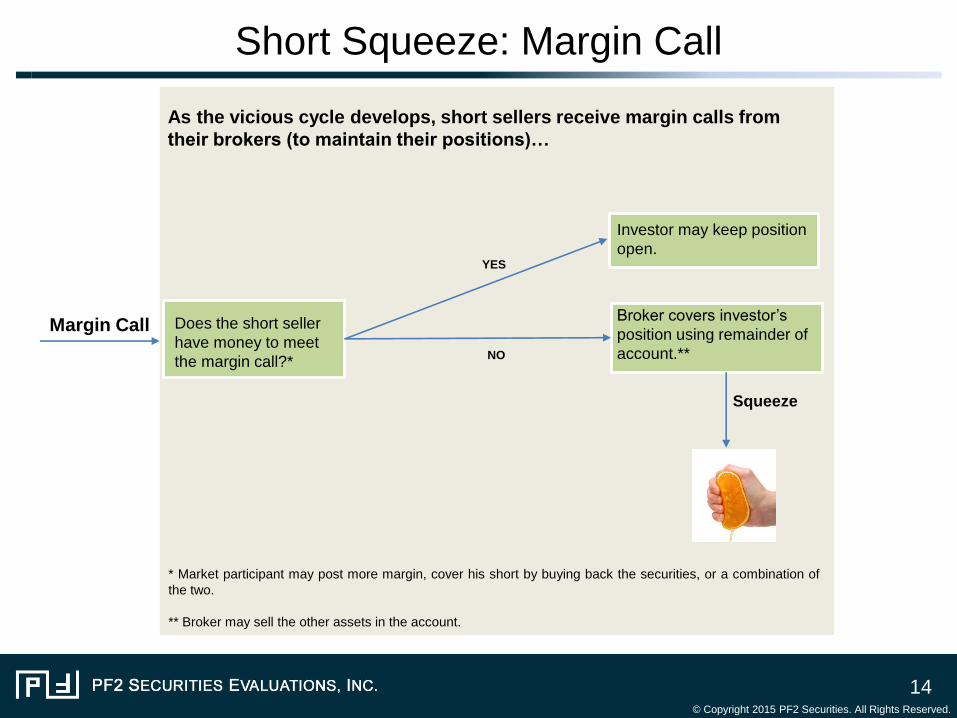

Short Squeeze: Margin Call

14© Copyright 2015 PF2 Securities. All Rights Reserved.

Margin Call Does the short seller

have money to meet

the margin call?*

Investor may keep position

open.YES

As the vicious cycle develops, short sellers receive margin calls from

their brokers (to maintain their positions)…

Broker covers investor’s

position using remainder of

account.**

* Market participant may post more margin, cover his short by buying back the securities, or a combination of

the two.

** Broker may sell the other assets in the account.

NO

Squeeze

Example: SNB Unpegs Swiss Franc

• Jan 2015: Swiss National Bank (SNB) decision to unpeg Swiss franc (CHF) from

euro (EUR) triggered massive rally in CHF.

• At one point CHF surged nearly 30% vs. EUR before stabilizing around a new

equilibrium price range.

• Unexpected and violent move inflicted large losses at many firms – sell-side &

buy-side. It also hit retail FX investors (and their brokers) with loses amplified via

leverage (up to 50x leverage at typical retail FX brokerage)

15© Copyright 2015 PF2 Securities. All Rights Reserved.

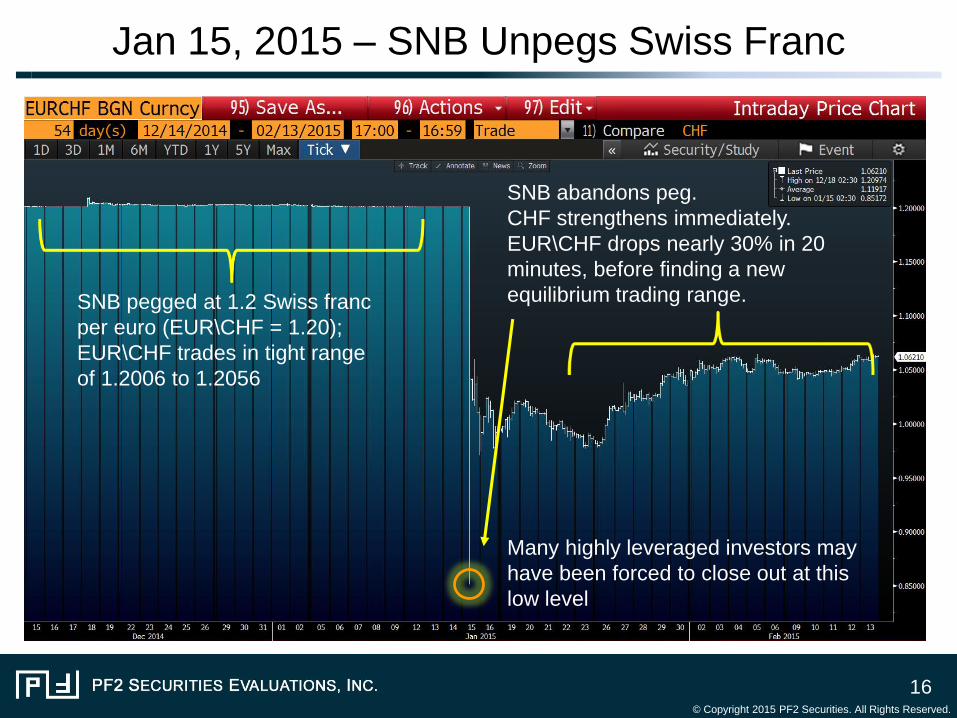

Jan 15, 2015 – SNB Unpegs Swiss Franc

16© Copyright 2015 PF2 Securities. All Rights Reserved.

SNB abandons peg.

CHF strengthens immediately.

EUR\CHF drops nearly 30% in 20

minutes, before finding a new

equilibrium trading range. SNB pegged at 1.2 Swiss franc

per euro (EUR\CHF = 1.20);

EUR\CHF trades in tight range

of 1.2006 to 1.2056

Many highly leveraged investors may

have been forced to close out at this

low level

20 Minute Move

17© Copyright 2015 PF2 Securities. All Rights Reserved.

EUR\CHF

pegged at

1.20

Euro falls over 29%

against the Swiss

franc in less than

20 minutes

EUR\CHF

pegged at 1.20

Euro falls almost 30%

against the Swiss franc in

less than 20 minutes

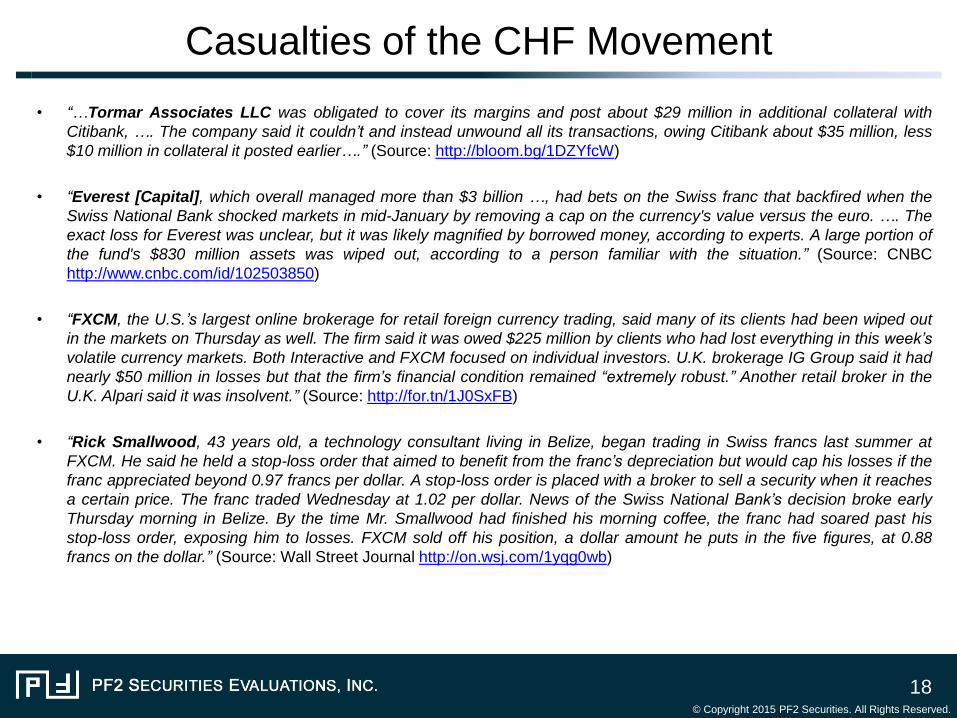

Casualties of the CHF Movement

• “…Tormar Associates LLC was obligated to cover its margins and post about $29 million in additional collateral with

Citibank, …. The company said it couldn’t and instead unwound all its transactions, owing Citibank about $35 million, less

$10 million in collateral it posted earlier….” (Source: http://bloom.bg/1DZYfcW)

• “Everest [Capital], which overall managed more than $3 billion …, had bets on the Swiss franc that backfired when the

Swiss National Bank shocked markets in mid-January by removing a cap on the currency's value versus the euro. …. The

exact loss for Everest was unclear, but it was likely magnified by borrowed money, according to experts. A large portion of

the fund's $830 million assets was wiped out, according to a person familiar with the situation.” (Source: CNBC

http://www.cnbc.com/id/102503850)

• “FXCM, the U.S.’s largest online brokerage for retail foreign currency trading, said many of its clients had been wiped out

in the markets on Thursday as well. The firm said it was owed $225 million by clients who had lost everything in this week’s

volatile currency markets. Both Interactive and FXCM focused on individual investors. U.K. brokerage IG Group said it had

nearly $50 million in losses but that the firm’s financial condition remained “extremely robust.” Another retail broker in the

U.K. Alpari said it was insolvent.” (Source: http://for.tn/1J0SxFB)

• “Rick Smallwood, 43 years old, a technology consultant living in Belize, began trading in Swiss francs last summer at

FXCM. He said he held a stop-loss order that aimed to benefit from the franc’s depreciation but would cap his losses if the

franc appreciated beyond 0.97 francs per dollar. A stop-loss order is placed with a broker to sell a security when it reaches

a certain price. The franc traded Wednesday at 1.02 per dollar. News of the Swiss National Bank’s decision broke early

Thursday morning in Belize. By the time Mr. Smallwood had finished his morning coffee, the franc had soared past his

stop-loss order, exposing him to losses. FXCM sold off his position, a dollar amount he puts in the five figures, at 0.88

francs on the dollar.” (Source: Wall Street Journal http://on.wsj.com/1yqg0wb)

18© Copyright 2015 PF2 Securities. All Rights Reserved.

Short Interest & Free-Float

• Short Interest: Total # shares sold short; also can be expressed as % of

total shares outstanding

• Free Float: # shares outstanding that are readily available to trade

(excludes restricted stock and closely-held shares)

• Useful measures to identify potential short squeezes (higher ratios

indicate greater potential for short squeeze)

• Short interest to free-float ratio

• Short interest to average daily volume ratio

• Coming soon… actively managed ETF will provide long exposure to

stocks vulnerable to short squeezes• http://www.etftrends.com/2015/04/issuer-putting-the-finishing-touches-on-short-squeeze-etf/

19© Copyright 2015 PF2 Securities. All Rights Reserved.

Porsche and VW

• 10/28/2008: For one day, Volkswagen was the world’s most valuable company(by market cap), following a massive short squeeze.

• The trigger was Porsche’s announcement that it had increased its stake in VWfrom 31% to 74%, primarily by exercising call options it had quietly accumulated,and thus shrinking VW’s free-float to around 6% of outstanding shares (the stateof Lower Saxony owned 20% of VW).

• Roughly 13% of VW’s shares had been lent out for short-selling: more thandouble the free-float of 6%. Investors rushed to cover their shorts, since therewere not enough available shares to cover all shorts. In just 2 trading days, VWshares soared from a close of €210.85 to €945, as shorts were forced to cover(at newly exaggerated prices).

• 10/29/2008: Porsche announced that it would sell 5% of its stake in VW,relieving the pressure of short covering (and also locking in some of Porsche’sprofits). Once there was no more forced short-covering, upward pressure on thestock abated & VW shares fell back to pre-squeeze levels.

20© Copyright 2015 PF2 Securities. All Rights Reserved.

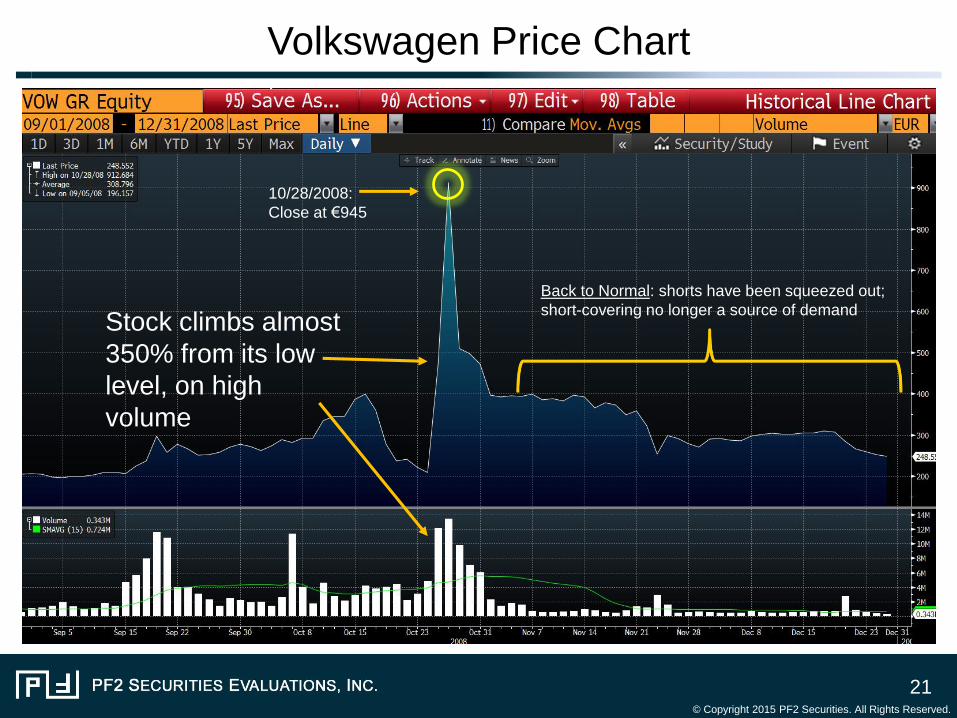

Volkswagen Price Chart

21© Copyright 2015 PF2 Securities. All Rights Reserved.

10/28/2008:

Close at €945

Stock climbs almost

350% from its low

level, on high

volume

Back to Normal: shorts have been squeezed out;

short-covering no longer a source of demand

Sears

• Sears Holding Corp (SHLD) exemplifies the ingredients for short-

squeezes.

• The company’s operational struggles were well documented: with 11

consecutive losing quarters as of 4Q14 (reported 2/26/2015), it was a

popular short target.

• But while the short interest was high at 10.3MM shares (as of 3/31/2015),

most of the 107MM shares outstanding were at the time closely held*,

leaving a free float of only 13.98MM shares

* CEO Eddie Lampert reportedly held ~51.7MM shares; Fairholme Capital Management (run by Bruce Berkowitz) reportedly held ~26.5MM shares

22© Copyright 2015 PF2 Securities. All Rights Reserved.

Sears – 11/7/2014

• Sears announced possible plans to set up REIT for a sale and lease-back of 300 stores,

freeing up much-needed cash. Shares bounced roughly 30% in the day, before slowly

returning to pre-short squeeze levels.

23© Copyright 2015 PF2 Securities. All Rights Reserved.

31% Pop